09/07/2020

09/07/2020

In February 2012, Shehata, 31 years old at the time, took out a life

insurance policy with the Egyptian Takaful Insurance Company (Hayat),

for 500,000 Egyptian Pounds (approximately $81,000 at the time). The

insurance money, to be paid-out to his family after his death, would

be in monthly instalments of E£7,560 (~$1,200). Six months later,

Shehata took out a second life insurance policy for the same amount.

Less than a year later, his family presented his death certificate to

the two companies, to collect the cash amount of both policies. This

raised suspicion and led the company to file a report with the

Administrative Control Authority and the Public Fund Investigation

Bureau against the heirs.

In addition to the death certificate, Shehata’s family presented a

medical report issued by a Health Department in the village of Bani

Mazar in Assiut, stamped with the Ministry of Health’s seal, and

signed by a health inspector. The report stated the cause of death as

hypovolemic shock caused by a heart attack. However, according to the

company’s managing director, Hisham Abdel Shakur, the prosecution’s

investigations revealed that Shehata was still alive, and that the

company had fallen victim to a mastermind fraud scheme, from which

Shehata and his family pocketed E£107,500 (~$17,500) — as a first

pay-out. He stated in a press conference that Shehata was part of an

organised crime ring of death fraud causing insurance companies losses

mounting to E£5 million.

ARIJ monitored deaths between 2012 and 2020, during which fraudsters

used fake medical reports and death certificates to reap millions of

pounds from life insurance companies. ARIJ’s investigation also found

how official documents are forged through the exploitation of

loopholes in the Civil Status Law, in order to obtain compensation.

This fraud prompted reinsurance companies to withdraw from the

Egyptian market after incurring financial losses, amid poor oversight

on the part of the Ministries of Health and Interior, as well as

regulatory bodies, and the absence of modern technological tools to

detect fraud and theft crimes.

A contract whereby the insurer is obligated to pay to the insured, or to the beneficiary, for whose interest the insurance contract was stipulated, a sum of money, a regular income, or any other financial compensation in the event of the occurrence of the accident, or of the risk stated in the contract, whether injury or death, in consideration of a premium or any other financial payment made by the insured to the insurer. The lump sum of the life insurance policy will only be disbursed in the event of death.

Source: The official website of The Egyptian Financial Regulatory Authority for 2019 Annual book 2018-2019

Head of the Insurance Department at Cairo University’s Faculty of Commerce, Sami Naguib, explains that there are two types of Insurance; the first, is the individual agreement through an insurance policy, whereby the insured pays a monthly premium, and the company pays him the cash value of the policy in the event of disability. The company will also pay his family the cash value of the policy after his death, provided that they present the death certificate and inheritance claim. He clarified that insurance pay-outs depend on the type of death, which would increase in the case of a "natural death" and would decrease in the case of a criminal death. The second type is the common social security that the state guarantees to all workers.

Annual book 2018-2019 (All amounts in E£)

According to Mahmoud Sami, secretary general of the Egyptian

Insurance Federation — a government federation that consists

partly of insurance companies — the percentage of losses from life

insurance fraud rose from 11% in 2017 to 18% during 2019, an

increase of 7% in a period of less than two years. While he

estimated the losses to have reached E£50 million in the last two

years, he described those losses as "small" compared to the size

of the insurance companies’ premiums.

The former head of The Egyptian Financial Regulatory Authority,

Sharif Sami, explained that the insurance premiums that those

insured pay periodically are one of the most important sources of

investment funding in the country. According to an information

bulletin issued by the Egyptian Insurance Federation on December

22, 2017, fraud is one of the most important challenges impacting

the insurance industryin Egypt, and 54% of life insurance

companies said that fraud constitutes the number one risk their

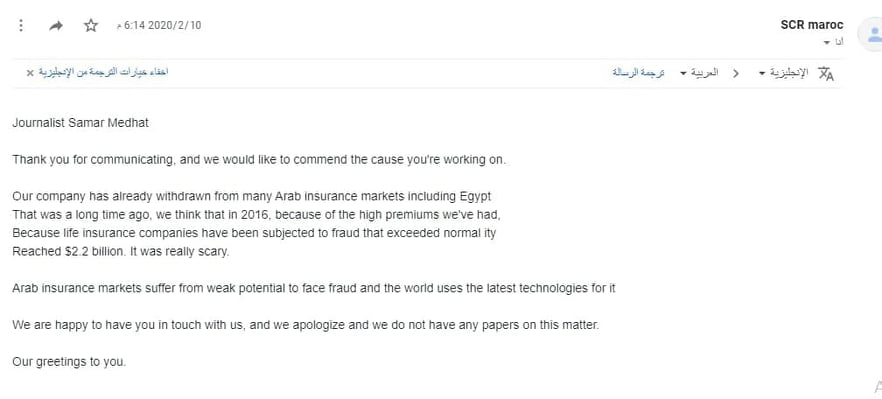

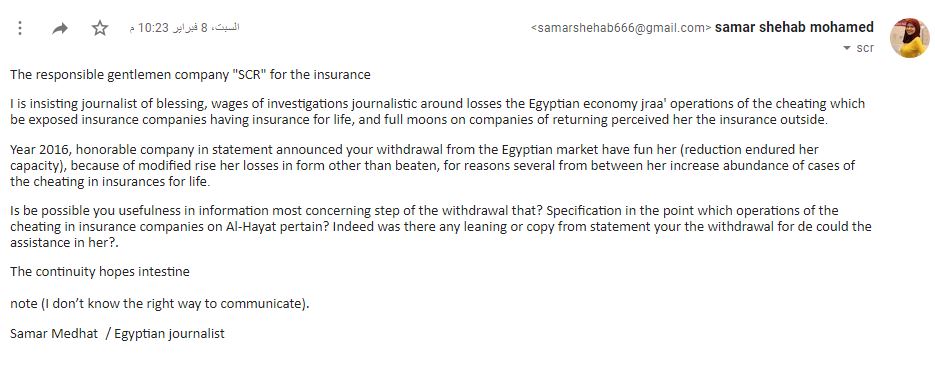

operations face. In 2016, the Moroccan Central Reinsurance

Company, SCR, withdrew from the Egyptian market. When asked for

the reason behind its withdrawal from the Egyptian insurance

market, the company’s representatives said that it was due to the

increasingly high premiums, and cases of fraud that exceed what

insurance companies were used to.

Source: The Egyptian Financial Regulatory Authority official website

In 2016, the Moroccan Central Reinsurance Company, SCR, withdrew from the Egyptian market. When asked for the reason behind its withdrawal from the Egyptian insurance market, the company’s representatives said that it was due to the increasingly high premiums, and cases of fraud that exceed what insurance companies were used to.

Reinsurance companies operating in the Egyptian market, according to the official website of Egypt’s Financial Supervisory Authority

Reinsurance companies are

global companies that contract Egyptian insurance companies, and

get a share of the insurance premiums in exchange for assuming

part of the cash value of the insurance policy after the insured

client’s death, or his exposure to any incidents that allow for

the disbursement of the funds...

The Moroccan company estimated life insurance companies’ losses at

$2.2 billion, and attributed it to the poor capabilities of

confronting fraudulent methods, as well as the backward technological

systems used.

Sami Naguib explained that to carry out insurance fraud, the fraudster needs a fake but documented and dictated death certificate with official seals, in order to present it to the insurance company and collect the value of the policy. The fraudsters will take all steps needed for issuing the certificate officially, however along the way he needs to falsify some of the steps or documents, as this investigation reveals.

Sources

1- Articles No. (4/28/386) of the Civil Status Law No. 143 of

1994.

2- Dr. Hassan Aref, Health Inspector Ms. Zainab.

In the event of a criminal death, the health inspector informs the

Public Prosecution, who assigns a forensic doctor to examine the

deceased and determine the causes of death.

Amid an unrelenting wailing, 35-year old Shalqami, asked the

inspector at the Bandar Al-Minya health office to issue a death

certificate for his wife, Amina, while presenting a false medical

report dated May 14, 2018, with no hospital notification of her

death. He explained that the hospital refused to give him the

notification for his wife’s death during an outpatient procedure of

"soft tissue" biopsy. (As shown in the case documents).

The health inspector eventually gave in to Shalqami’s begging and

issued the death certificate and burial permit, without seeing any

hospital documentation or official notification.

Article 40 of the Civil Status Law states: “The employee of the competent health authority receiving death notifications must verify the identity of the deceased, and complete the data and documents required to confirm the death.”

Head of Bandar Al-Minya Health Office, Hani Ishaq, says that by

reviewing the civil death registry during the year, he found the

woman’s name and death-related documents, but did not find the

notification which the University Hospital usually sends to the

health office after a death.

Ishaq filed a report with the Public Prosecution office for the year

2018, after the husband requested that the Health Office issue a

cause of death document, to present it to Nasser Social Bank (a

government bank), in order to collect the value of an insurance

policy in the amount of E£100,000, which Amina did not pay off

before her “death” .

Investigations conducted by the prosecution revealed that the woman

was still alive and had moved from the Minya Governorate to the

Hawamdiya area in Giza, after the husband faked a University

Hospital medical report and a health inspector assisted him in

issuing the death certificate without a hospital verification.

The husband was sentenced in absentia to 20 years in prison, while

Amina was sentenced to 10 years. They had already collected nearly

E£250,000 from a loan, the insurance policy, the end of service

bonus and the government pension for several months. The health

inspector was sentenced to three years, according to the case

documents and Hani Ishaq.

Health offices of the Preventive Medicine Department in Egypt’s

Ministry of Health and Population, in all governorates of the

republic, are the main source of data related to more than 100

million Egyptian citizens, and are responsible for issuing birth and

death certificates, as regulated by Law 143 of 1994.

“Falsification of the death certificate passes through three people:

the insured, a health inspector, and a broker/intermediary between

them,” explains Dr. Hani Ishaq, the health inspector of Bandar

Al-Minya, and the former head of the Governorate's Free Therapy

Department.

Ishaq says that a loophole in the Civil Status Law allows health

inspectors to register deaths based on medical reports from

government hospitals, private hospitals, or a private doctor, which

allows for more tampering with the death registration.

Ishaq points out that these medical reports are easy to tamper with

and forge. In cases of home deaths, the health inspector must

examine the body and verify the death and its cause. However, this

does not happen often. Ishaq attributes this to the fact that a

health office records between 15 to 20 deaths per day, whether death

occurs at home or at a hospital, were due to an accident, or

criminal activity.

Hassan Aref, a retired health inspector who worked for years in the

office of Sayyida Zainab confirms Ishaq’s statement. In an interview

he said: “85% of health inspectors do not personally perform a

medical examination on the deceased to verify the cause of death and

the identity of the deceased. They issue the burial permit and the

medical report from their offices."

However, negligence is not the only cause. Ishaq accuses "some

health inspectors of participating in fraud and accepting financial

bribes ranging between E£100 and E£500, to issue death certificates

without verification, notifications or entries in the death

registry," all this, in the absence of periodic monitoring and

inspection from government agencies.

Ishac chaired a committee to screen death certificates in Minya

Governorate, which found that 36 false death certificates were

issued during 2016 and 2017.

In March 2020, police report No.1195 of 2020 from Sayyida Zainab,

supported Ishaq’s findings, as it revealed that employees of the

Sayyida Zainab Health Bureau issued a false medical report, a burial

permit and a fake death certificate for a person named Shawish, to

collect the cash value of an insurance policy in the amount of E£20

million ($1,300,000), collected by the person who staged the "fake

funeral" himself, a month before reporting his death. Investigations

are still ongoing.

When confronted, Mohamed Abdel-Fattah, head of the Central

Department of Preventive Medicine at the Ministry of Health and

Population, the department which monitors the work of health

offices, did not deny the involvement of some health inspectors in

tampering with death certificates: “There are definitely the weak

spirited, and the fraudulent here an there and they will continue as

long as the human element is controlling the system.”

Abdel Fattah added that the plan to digitize health offices date

began in February 2020. It aims to transfer all paperwork

transactions from paper to electronic, to curb fraud and corruption

in death and birth registration. He stressed that the electronic

transformation will reveal falsification and fraud attempts of

official documents in health offices.

In February 2020, the Ministry of Health announced the automation of

4,571 health offices in Egypt tasked with registering births and

deaths.

We contacted a mediator or a so called broker involved in issuing official forged documents. During several recorded phone calls, we requested a death certificate for a person who is still alive to present to an insurance company. His response was that for E£25,000 ($ 1600) he could provide a death certificate sealed with the stamp of the Ministry of Health from a health office, but it would not be recorded in the civil registry. We requested that he records it in the civil registry, and he said: "I will try."

An easier way for the mediator would be to issue a death certificate not entered in the civil registry, but stamped with the seal of the Ministry of Health, obtained through "one of his friends", as he puts it, in one of the health offices. The broker recommended presenting it to the company and attributing the lack of entry into the registry to the slow pace of procedures. He insisted that in the end, the company will accept the certificate because of the stamped seal of the Ministry of Health and its approval by the Health Office.

The manipulator of birth and death certificates shall face

imprisonment for a period not exceeding three years or a fine of

no less than E£500 ($30), and anyone who falsifies procedures

related to death and inheritance shall face imprisonment for a

period not exceeding two years or a fine not exceeding E£500

($30).

Article 222 of the Penal Code stipulates that every doctor or

surgeon who gave by way of courtesy a false certificate,

statement, or report regarding pregnancy, illness, impairment,

or death, knowing that it was false, shall face imprisonment or

pay a fine not exceeding E£500 ($30). However, if his intention

in preparing a false report was in exchange for a bribe or

gifts, he will face life imprisonment and a fine of not less

than E£1,000.

Mohamed Othman, an insurance examiner at Misr Insurance Company told

us that in 2013 within the Sharkia governorate, Essam’s family

presented to Misr Insurance Company - the oldest state-owned life

insurance company - a death certificate accompanied by the health

inspector’s "natural death report”, and requested a payment of E£5

million (~$740,000 at the time), which was the cash value of an

insurance policy. Essam had only paid off E£200,000 (~$29,000 at the

time) in premiums, before travelling to Italy, where he supposedly

died.

Essam’s family collected E£3 million, as a first payment of the

policy’s cash value, pending the completion of related documents.

Othman said that because the death was “natural”, the death

certificate was sent to the investigation department in the

insurance company to verify the authenticity of the certificate,

only to discover after investigation, that Essam was still alive.

He added that in 2013, the company sued Essam’s family before the

Cairo Criminal Court, for falsifying official documents. In 2015,

they were sentenced to six years in prison, according to Othman.

Othman points out that the investigation department of the insurance

companies undertake verification steps related to the authenticity

of the policy holder’s death from the beginning to the end, they

make enquiries at his place of residence and at his workplace. He

explains that the Ministry of Interior is involved only in the event

of the invalidity of the death certificate, where the case is

referred to the prosecutor’s office for further investigation, which

in turn assigns it to the criminal investigations department for

examination and investigation.

He added that the Department of Investigations carries the same

duties as that of a criminal investigation, in inquiring about the

deceased and the authenticity of the documents presented. Their work

begins when the company’s management deems the claim as

“suspicious”, due to the short period of time that has lapsed

between the date of taking out the insurance policy and the reported

death. An investigation is carried out by the administration to

verify the death certificate and the burial permit, without

resorting to agents of the law unless the suspicion of fraud are

proven to be correct.

However, a security source in the civil status department, who

requested to speak anonymously, said that the Civil Status

Inspection and Monitoring Unit, accompanied by the Criminal

Investigation Unit of the police, routinely conducts unannounced

visits to branches of the civil registry offices to check for any

violations, adding: "Cases of forgery of official documents are

usually committed by individuals and not the system. Forgery and

bribery cannot be controlled,” attributing it to poor oversight.

He added: "Some employees forge seals, so that the forged documents

appear authentic." He said that the Ministry of Interior has a plan

to transform 90% of daily processes into electronic form, explaining

that the digital system reduces the forgery or the issuing of

fraudulent documents.

“The law does not protect the dupes,” explains Subhi Shehata, a

member of the Public Relations and Media Department, of The

Financial Regulatory Authority, responsible for supervising and

regulating non-banking financial markets and instruments, including

the insurance sector. He denied the authority’s involvement in

handling fraud on behalf of insurance companies: “There is no

regulatory entity in the world that can verify the death is real, it

is not the authority’s job to verify the authenticity of the

document or the validity of the compensation.”

He explained that one of the roles of the Financial Regulatory

Authority is to resolve contractual disputes and complaints between

those who are entitled to insurance payments and companies. He said

that he Authority received 600 complaints in 2016 and 2017, the

majority of which relate to the companies' delay in disbursing

insurance pay-outs, approximately 90% of which the authority ruled

in favour of insurance companies.

He further added: "Every company that has a criminal intelligence

and legal affairs department, and a disbursement unit, should be

held accountable in the event of unlawful pay-out,” and stressed the

need to hold the managing director and the board of directors of

such companies accountable, or recourse to the judiciary and not to

the financial authority.

In reality however, fraudsters will continue to pocket huge amounts

in life insurance pay-outs; and insurance companies will continue to

suffer losses; and the cost of life insurance for Egyptians will

continue to rise as long as the mechanism to commit fraud using

falsified documents to obtain life insurance policies pay-outs

continue to thrive within Egypt.